The Division 293 tax in Australia is a tax rule that targets higher-income earners by applying an additional tax rate on their superannuation contributions. It aims to make the tax treatment of superannuation fairer and ensure that high-income individuals receive the same concessional tax treatment as lower-income earners.

Who Does It Apply To?

The Division 293 tax is applicable to individuals whose combined income (including taxable income and concessional superannuation contributions) exceeds a certain threshold.

For the 2022-2023 financial year, the threshold is set at $250,000.

To calculate the Division 293 tax, you need to determine the excess amount above the threshold and apply a 15% tax rate to that excess.

ATO assess you for Division 293 once you have lodged your Individual Tax Return AND your superfund(s) have lodged their returns confirming your contributions.

How to Pay?

Division 293 Assessments are issued to you as an individual. As Div293 imposes an extra 15% tax on some or all of your super contributions for a given year.

There are 2 ways to pay:

– from your own money; or

– by releasing money from your super

We recommend releasing money from super as the funds being taxed are sitting in super.

EXAMPLE

Let’s take the example of someone earning $240,000 with $19,000 in super contributions in the same year.

Step 1: Calculate the combined income

Combined income = Taxable income + Concessional superannuation contributions In this example, the taxable income is $240,000 and the concessional superannuation contributions are $19,000.

Combined income = $240,000 + $19,000 = $259,000

Step 2: Determine the excess amount above the threshold

Excess amount = Combined income – Threshold In this example, the threshold is $250,000.

So, in this scenario, an individual earning $240,000 with $19,000 in super contributions would be liable for a Division 293 tax of $1,350.

Division 293 assessments are issued to the individual in a similar way to a regular Notice of Assessment. The assessment will come via myGov or via mail. You need to deal with this straight away.

We recommend following the instructions to have money released from super to pay the assessment before the due date.

DISCLAIMER: It’s important to note that this is a simplified example and actual tax calculations may involve other factors and deductions. It’s advisable to consult with a qualified tax professional or the Australian Taxation Office (ATO) for accurate and personalized tax advice.

If you’re an individual or sole trader, you can manage your tax and super online.

To do this, you will need a myGov account linked to the ATO. To get started, you should have the following.

A myGov account using SMS,

myGovID or

the myGov code generator app as your sign in option,

your tax file number TFN.

And two of the following.

A notice of assessment received in the last five years.

A PAYG Payment Summary received in the last two years.

A super account statement from the last five years.

A dividends statement from the last two years.

A Centrelink payment summary from the last two years.

Or your bank account details. This must be an account you had your income tax return refund paid into last year or has earned interest in the last two years.

If you don’t have this information available, you will need to phone the ATO and get a unique linking code to complete this process.

Once you have this information ready, visit my.gov.au and sign in to your account.

When signed in, go to the linked services section and select view and link services. In the link a service section, select the link button to the right of Australian Taxation Office.

When you link the ATO, myGov will store your name and date of birth in your profile. If you already have a profile, these details must match, read and agree to the ATO terms and conditions. Provide your details, including your tax file, number, name, date of birth and address.

If your details have changed since you last dealt with the ATO, you will need to phone to update them before you can complete the link. Enter information carefully and accurately so that it will match your details held by the ATO.

You will also need to answer two questions from information contained in documents mentioned earlier. If you receive an error message at any time, take note of the error code and follow the link or instructions for more information. Once you’ve finished answering these questions, you’re done.

You have successfully linked your myGov account to your ATO record and that’s it. You can now manage your tax and super affairs through ATO online.

We break it down to explain what fringe benefits tax is, who can get the exemption, and why the Electric Vehicle (EV) exemption is such a good deal.

Federal and State Governments in Australia are now offering incentives to encourage the uptake of zero-emission vehicles. The Federal FBT Exemption is the biggest incentive available at the time of writing this. This can give you roughly a 40% discount.

Did you know you can now get a Tesla for less than a Toyota Corolla?

You need satisfy 3 main elements to qualify:

You must be an employee or an associate of an employee

Select an EV that qualifies by price and first use date

Have your Employer provide the EV to you as a Fringe Benefit –

commonly organised via a Novated Lease for employees

small business owners – speak to your accountant

BENEFITS:

Assuming you have satisfied the above points you can:

Save TAX – by having the cost of the car come out of your pre-tax income, regardless of your work usage of the vehicle.

Avoid paying for fuel into the future and the stress of fuel price fluctuations.

Save GST

Get a $67,000 EV for less than a $36,000 Internal Combustion Engine (ICE) car. See our example below

Potentially get State Government incentives that waive or reduce stamp duty – check your state rebates below:

Mining, transport and refining of fuel is not required

No fine particle emissions from exhaust fumes

Common Concerns with EVs

Humans are creatures of habit. Any change comes with concerns but we have found that the benefits of EV adoption far outweigh any concerns people may have.

Where do I charge? Most people plug into a regular power point at home. This adds about 120km of range over night via a regular 10 amp power point. You can get faster charging setups at home if required.

How far does the car go on one charge? Most new EVs have a range of 300 – 500km on a full battery, depending on the make and model and size of the battery. Tesla Model Y RWD has a range of 432km for example with a 60Kwh battery. Similar to a tank of fuel.

EVs Cost Too Much. We agree they are expensive upfront. This is why the FBT exemption is so good. This reduces the total cost of ownership by around 40%. Like all new technologies they start out very expensive and reduce in cost over time. Like flat screen TVs did a decade ago.

There are not many EVs Available: True, for now – there are about 14 Battery EVs available in Australia in Feb 2023 in the $40k to $80k price range that will be possible to acquire with FBT Exemption. Vehicle manufacturers are ramping up their range so many more will be available in the coming years.

Can I go on road trips? Yes! Absolutely. There is an extensive network of fast chargers around Australia. Fast chargers can add 80% battery charge in under 15 minutes. Tesla is opening it’s industry leading supercharger network to non-Tesla EVs as well.

Can I Tow?: Yes but this will reduce range just like it will in an ICE vehicle. There are some bigger towing vehicles coming but they are likely to be more expensive than the LCT limit.

Won’t the battery die in a few years? No. New battery technology allows for 10,000 charging cycles. So batteries will likely outlast the vehicle itself.

We have staff who have already taken advantage of this amazing deal so we have real world experience. If you are interested please read the details below.

DISCLAIMER: Please note that the financial examples provided on this page is for illustrative purposes only and should not be construed as financial advice. The figures and calculations used may not be accurate or applicable to your specific financial situation. It is important to seek professional financial advice before making any investment decisions. The author and publisher of this example shall not be held liable for any damages or losses incurred as a result of using the information provided.

Electric Vehicle Charging Image

What is a Fringe Benefit?

FBT, or Fringe Benefits Tax, is a tax system in Australia that applies to non-cash benefitsprovided to employees or their associates as part of their employment. These benefits can include things like company cars, health insurance, and expense accounts, among others.

FBT is an important part of the Australian tax system, as it helps to ensure that employees are not receiving excessive tax benefits through their employment arrangements. It also helps to maintain fairness in the tax system, by ensuring that all employees are subject to similar tax obligations regardless of their employment arrangements.

When an employer provides a fringe benefit to an employee, they are typically required to pay FBT of 47% on the taxable value of the benefit. However, if the employee makes an employee contribution towards the cost of the benefit, this can reduce the taxable value of the benefit and therefore reduce the amount of FBT that the employer is required to pay.

For example, if an employer provides an employee with a company car, they may be required to pay FBT on the value of the car. However, most workplaces require employee to make an employee contribution towards the cost of the car to eliminate any FBT that the employer may have been required to pay.

How Does This Apply To Electric Vehicles?

Like everything relating to tax, it is a bit complicated.

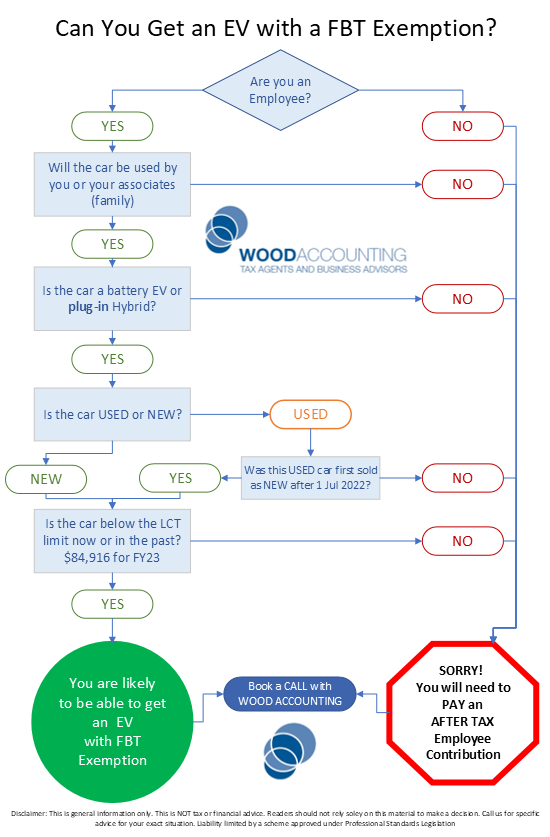

To get an EV as an FBT Exemption you must meet ALL of the following criteria:

✅The vehicle must be zero or low emissions.

✅The first time the vehicle was held and used by ANYONE must be after 01 July 2022

✅The car is used by an employee or their associate (ie family members)

✅Luxury Car Tax (LCT) has never been payable on the importation of the vehicle.

We quickly expand these points below

1- What is a Zero or Low Emission Car?

Good question. Also complicated.

ATO defines Zero and Low Emission cars this as follows:

It is a:

Battery Electric Vehicle (BEV)

hydrogen fuel cell electric vehicle, or

Plug-In Hybrid Electric Vehicle (PHEV)

MUST BE PLUG IN – not just a “hybrid” that charges off the petrol engine.

Plug-in Hybrid exemptions EXPIRE 31 March 2025.

It is a car designed to carry a load of less than1 tonne and fewer than 9 passengers (including the driver). Above 1 tonne and/or 9+ passengers are Non Cars and no FBT Exemption applies.

Motorcycles and scooters are not cars for FBT purposes and do not qualify for the exemption, even if they are electric.

2 – First Used after 1st July 2022

Basically the vehicle must have been first purchased NEW on or after 1 July 2022.

This means the exemption would NOT apply to the purchase of a 2nd hand vehicle that was first used before 1 July 2022.

So to be clear here are 2 quick examples:

Buy a used 2019 Tesla Model 3 in December 2022. This car was first registered and used in 2019 – FBT Exemption DOES NOT apply – as first use was before 1/7/22.

Buy a used 2022 BYD Atto 3 in Feb 2023. This car was first used in October 2022. You can get the FBT Exemption on this vehicle as it was first used AFTER 1/7/22.

3 – Car Must Be Used by an EMPLOYEE or Their Associates

This is important.

There must be an Employer – Employee relationship in order for a Fringe Benefit to arise.

The exemption only applies during the employment relationship. I does not apply before or after an employment arrangement is active.

SOLE TRADERS do not qualify as they are NOT employees.

Quick definitions:

Employer = The entity with which an employee has a contract to provide their labour. Written or otherwise. Usually a company or trust which would provide the employee with a payslip, super etc.

Employee = A human who has agreed to work for an entity. Self employed people are included here AS LONG AS they are an employee of their own company or trust.

Sole Trader = Human who has an ABN and works for themselves, issuing invoices for work. Not on payroll. Can’t provide a Fringe Benefit as there is no employee/employer relationship.

4 – Below Luxury Car Tax (LCT) Limit

To be eligible for the FBT Exemption, the value of the car MUST have been below the LCT threshold for fuel efficient vehicles:

at the time it was a new vehicle,

AND in any subsequent sale

If you buy a 2nd hand EV you will need to get confirmation that it was NOT subject to LCT at any time in the past.

Small Business Owners – If you use a company or trust structure and pay yourself or family wages, talk to us or your Accountant, to confirm that you qualify.

For employees – speak to your HR department or your boss to confirm that you are able to salary sacrifice a novated lease. Then contact the novated lease provider to organise the car.

Sole Traders – sorry, you don’t qualify. FBT does not come into it for you. Your vehicle tax deductibility is assessed by logbook business use percentage.

Example: Comparison of Novated Lease for Electric Vehicles

Electric Vehicle (EV) vs Internal Combustion Engine (ICE) vehicles.

Mr Wood is looking for a new car. He has rounded it down to 2 of the top selling vehicles in Australia in 2022.

Mr Wood’s circumstances are as follows:

Self employed on wages

Full time earning around $100,000 gross per year

Employer agrees to salary sacrificing a novated lease

Has had the same job for 2+ years and has a mortgage on a home for 2+ years as well – banks and novated lease companies want to see this most of the time.

Both cars are new purchases AFTER 1 July 2022

Both cars are under the Luxury Car Tax (LCT) limit – $89,332 for fuel efficient EVs or $76,950 for other vehicles in FY 2024.

Running costs to be part of the packaged repayments.

Employer or novated lease company will reimburse the costs of charging at home as an expense claim. Subject to negotiations.

Toyota Corolla

Tesla Model 3

Driveaway Price – estimated at Feb 2023

$36,500

$67,485

Est. Running Costs – rego, ins, fuel/power, repairs

$5,500

$4,500

Est. Loan repayments – 60mths, no residual @8%

$8,881

$12,348

Total Estimated Running CostsPer YEAR

$14,381

$16,848

——–ANNUAL PAY AFFECT for Salary Sacrifice——–

Employee Taxable Income

$100,000

$100,000

Less: Pre Tax Deduction

($6,716)

($16,848)

New Taxable Income

$93,294

$83,152

INCOME TAX WITHELD

($22,650)

($19,154)

Less: Post Tax Deduction – Statutory Method

($7665)

($0)

Net Income to Bank – per year

$62,969

$63,998

EV vs ICE Novated Lease example

Conclusion

The above example, using real world numbers, shows that you can get a relatively expensive EV for less than an ICE vehicles despite the drive away price being so different.

Before considering an EV, Mr Wood was earning $100,000 gross income, less $25,000 tax withheld, resulting in him receiving $75,000 into the bank after tax.

Tesla – After pre-tax deductions and tax the income to bank for Mr Wood is $63,998. So compared to the $75,000 above, the Tesla option costs $11,002 out of pocket per year.

This car would have cost him $16,848 after tax had he not salary packaged. $5846 saved per year. This would reduce the cost of the car by more than $29,000 over 5 years. A massive 40%+ saving on the original price of the vehicle.

Corolla – After pre-tax deductions and tax the income to bank for Mr Wood is $62,969. So compared to the $75,000 above, the Corolla costs Mr Wood $12,031 per year.

This would have cost him $14,381 after tax had he not salary packaged. $2,350 saved per year.

So which one is cheaper? The Tesla. Why? This is due to the FBT Exemption. Mr Wood would have a lower out of pocket cost per year.

This is an example so please do your own calculations or ask an expert to assist you to make a decision.

What Else Do You Need to Know?

Your employer still needs to calculate a Reportable Fringe Benefit Amount (RFBA) and report this on your Annual Income Statement to ATO via Single Touch Payroll. You do not pay income tax on this amount, but it does impact income tests for child support, family assistance, HECS, Medicare Levy and some other Government benefits.

RFBA for exempt EVs does not impact FBT liability for the employer. It is also not included in:

certain non-profit employers – The $17,000 or $30,000 exemption cap

for rebatable employers – the $30,000 rebate cap

The Government will review this exemption by mid-2027 to consider EV take up and decide if the exemption continues.

Installation of an electric vehicle charging station in the home of the employee is NOT FBT Exempt. That is a property fringe benefit to the employee.

TESLA REFERRAL BONUS – If you are thinking of ordering a Tesla you can get a discount or referral points by using our referral code. We get referral points and you get a discount. Everyone’s a winner.

DISCLAIMER: Please note that the financial examples provided on this page is for illustrative purposes only and should not be construed as financial advice. The figures and calculations used may not be accurate or applicable to your specific financial situation. It is important to seek professional financial advice before making any investment decisions. The author and publisher of this example shall not be held liable for any damages or losses incurred as a result of using the information provided.

Having your full name correct with Governement agencies has never been more important.

In light of recent data breaches at large companies, like Optus and Medibank Private, ATO have increased their security around ANY changes to cleint names.

Tax Agents can no longer assist in the name change process – this is to ensure the actual person is changing their own name. Cases have surfaced of Tax Agents being instructed to change names by other family members or business associates without the actual person being aware. Driven by identity theft of fraud.

How Do You Change Your Name With ATO then?

You will need to gather some basic infortmation to allow the change to happen:

Your full name

Your Date of Birth

Your current home address

Your Tax File Number (TFN)

Your last tax refund or payable amount – should you not have that they will ask other questions realting to your tax return. Your employment income etc.

Your MARRIAGE CERTIFICATE, CHANGE OF NAME CERTIFICATE or DIVORCE ORDER as evidence. This must be the actual marriage certificate. Not the ceremonial one. See below.

Have your most recent Notice of Assessment from ATO handy.

ATO will need the Registration Number from the top right corner of your marriage certificate

If ATO already have your mobile number on file they can send you a 6 digit code as a 2 factor authentication

Other Name Change Reasons

You may have other issues with your name at ATO such as:

Missing middle name

Mispelt name

Short name vs full name – eg Ben vs Benjamin

Australianised name vs your birth name. Frank with ATO but Fotios on birth certificate.

Changing your name by choice

Why Does All This Matter?

As ATO and other Government agencies digitise and consolidate their databases they have multiple instances of each person across their different systems. Some of these have incorrect data such as names. MyGov and MyGovID are being used to centralise the identity of the human interacting with Gov to give both you and the Gov certainty that only you can access and change your own data.

Changing your name is hard because it should be hard. Having tight portocols around name changes makes it hard for fraud and identity theft to happen in the first place. This is a good thing.

Protect your private information as the experience of having your identity compromised or stolen is very traumatic and time consuming to correct. In some cases it can’t be entirely corrected.

Do you need extra funding to take the next step in your business strategy? We’ll help you review lenders and finance products – so you can find the best finance option for your business. #businessadvice

Every business needs finance to get the initial enterprise off the ground. You may well have entered into finance arrangements to fund the initial stages of the business, taking out loans to purchase equipment, lease premises or take on staff.

When was the last time you reviewed your finance or looked at the options for accessing other routes to funding? Are your finance facilities still offering the best interest rates and repayment terms, or are there better deals out there?

Other finance options may be available to help you fund your continuing growth, so taking a look at the current finance market is well worth thinking about.

Refinance your existing loans

It’s possible that you already have business loans in place. Sourcing that initial capital is such an important part of the startup process, and a vital stepping stone in getting your business idea operational. When was the last time you reviewed these finance arrangements? Could you, in fact, be getting a better deal?

The finance market is always evolving. New challengers will enter the market, new specialist finance products will be introduced and interest rates and repayment schedules will fluctuate and change. You may well have got a great deal on the business loans you took out five years ago – but refinancing these existing loans is likely to have multiple benefits.

You could:

Consolidate your existing loans into one finance facility

Lower the interest rate you’re currently paying on the loan

Pay off your loan more quickly, to reduce the debt in the business

Improve your cashflow position by cutting your repayment expenses

The key point here is that your business finance shouldn’t sit still. A loan is not a static debt. You can revisit and refinance your debt so it works in the best interest of the business.

Look for alternative routes to finance

Traditionally, businesses went to their bank manager when additional funds were needed. But the dynamic in the funding market has changed dramatically in recent years. Due to economic pressures, and the impact of the pandemic, the big banks have scaled back their lending to small businesses. Your high street bank is no longer the first port of call when finance is needed.

On the flipside of this, there are a growing number of alternative lenders, smaller challenger banks and specialist finance providers to choose from. And this has created a wide choice of different finance products to fit the needs of your growth plan.

If you need new equipment, asset finance is available.

When you have a short-term cashflow crisis, invoice finance is a good option.

If larger premises are needed, there are commercial mortgages to consider or bridging loans to make the initial purchase while you source the full capital that’s needed..

Explore the tax deductions that are open to your business

Another element of government-back financial support is the use of tax relief. One of your major expenses as a business will be paying your tax. There are usually various tax deductions available to help you reduce your tax bill and reinvest that saved money back into your business. Careful use of these tax breaks can make a big difference to your finances.

For example, Australia has research and development (R&D) tax relief scheme. To encourage businesses to innovate and invest in R&D, the government will offer a relief against the company’s expenditure on operational R&D costs. This may result in getting an R&D Tax Offset for your company. May rules apply to this so check with us or have a look at https://www.ato.gov.au/Business/Research-and-development-tax-incentive/

Another example is the Temporary Full Expensing of assets purcashed for business purposes. Temporary full expensing supports businesses and encourages investment, as eligible businesses can claim an immediate deduction for the business portion of the cost of an asset in the year it is first used or installed ready for use for a taxable purpose. More info on ATO website here

Choosing the right funding and finance will be vital to your long-term success as a business – so work closely with your advisers and think carefully about your choices.

We can recommend trusted finance brokers to assist with this process.

Banks and other lenders offer a variety of loans, so make sure you investigate your options and find a loan that suits the needs of your business.

Deciding how

much to borrow

Consider what source and type of finance will suit

your needs. The method of funding and term of the loan should match the

purpose for which the loan is being used.

Think realistically when assessing your financial

needs. Consider initial set-up costs. Estimate how long before your

business is likely to be self-supporting. You should be able to

demonstrate that you will be able to repay the loan, taking into account

potential risks such as lower than predicted sales or interest rate increases.

Applying for

a loan

If you are starting up a new business and need to

apply for a loan, the lender will require the following information from

you:

A description of the products and/or services you intend to

provide

A marketing plan showing how you intend to bring in business

Evidence of the demand for your products and/or services.

You will also need to provide details of your own

qualifications (both business and educational), previous business experience

and past achievements.

Obviously, the amount you need to borrow and the

purpose for which the loan would be used will need to be communicated to the

lender, and repayment terms will need to be clearly established.

If possible, financial information such as sales and profit projections over the term of the loan should be provided to the lender together with a cash flow forecast, showing the loan repayments, for the 12 months ahead.

Likely, the lender will seek security from you to

protect the loan and this can vary from one lender to another and will depend

on the type of loan and amount to be borrowed. Some generally acceptable

forms of security are:

real estate

shares in public companies

a personal guarantee.

Your loan application is more likely to be successful

if you provide the lender with a well written Business Plan which

includes:

your business goals and objectives

results of your market research which support your financial

projections and anticipated borrowings

systems you intend to implement to enable you to monitor your

business and respond to changes in your financial position.

YOUR ACTION PLAN

Have your Business Plan ready.

Prepare financial information including a cash flow forecast.

Seek expert advice. We can assist you.

Decide on a form of security

Speak with a finance broker

Contact Wood Accounting team today. We have numerous finance broker connections who are experts in Business Finance

For our current Xero clients we are working through our list and offering assistance, for a small fee, with reviewing payroll and registering for STP.

Single Touch Payroll explained

ATO also have a comprehensive section of their website dedicated to STP. We welcome STP as we feel this will even the playing field for businesses. STP will force ALL businesses to report their PAYG tax and Super obligations to ATO each pay run rather than at end of quarter or end of year. This will give ATO more visibility on those employers not meeting their obligations allowing them to take earlier action against those breaking the rules.

Buying an existing business offers a sense of security

because you have a good idea of what you’re getting for your money.

Existing customers and goodwill

An established business will generally come with

existing customers, clients, suppliers and staff. This eliminates much of the

effort and expense needed to generate goodwill, branding, advertising and

hiring staff.

Expenses and finance

The business is already operational and stock is

already on hand, so your initial expenses would be minimal and you can quickly

generate a cashflow. If you need to obtain finance, it may be easier because

the business has a proven track record.

Training and assistance

First-hand experience is valuable and the previous

owner and employees remaining with the business are best placed to give you the

training and assistance you need.

Disadvantages

An existing business does not come with a guarantee of

future success!

Goodwill may not last

There’s a risk that customers and clients may leave

when the business changes hands. Staff may wish to leave too and you may have

to pay their entitlements, such as long service leave. The departure of the

owner may have a negative effect on the business, so you can’t necessarily

guarantee the profits.

Reputation

The business may have a bad reputation or have made a

poor impression in the past – this might prove difficult for you to turn

around.

Premises and equipment

The premises may be inadequate and the equipment or

stock may be out dated or in need of replacing or repair.

YOUR ACTION PLAN

Thoroughly research the business!

For expert advice on buying a business, make an appointment to talk with your accountant, solicitor or business adviser.

Contact Wood Accounting team today on 02 95482828 for assistancewith this Action Plan!

Xero is an online accounting system that runs in your web browser on any internet enabled device. You can run your business accounting functions from your smartphone or tablet. Invoice, quote, track expenses without having to install any software.

We recommend Xero as it is tried and tested solution that suits almost all businesses big or small. We use it in our business.

Xero is the future of accounting. Get on board and change the way you do business.

Converting is simple!

•Optimize your current file – ensure debtors and contacts are up to date,

•have us review your file,

•pick a conversion date and we are ready to go.

Register your interest here and we will contact you to organise a needs analysis and a quote. Once we have your file it should take less than 4 days to have you fully operational in Xero.