Investing in property can be a lucrative way to build wealth, but it’s essential to understand the tax implications to maximize your returns. This guide will cover the full life cycle of property investment taxation for new investors

Investing in property can be a lucrative way to build wealth, but it’s essential to understand the tax implications to maximize your returns. This guide will cover the full life cycle of property investment taxation for new investors

In today’s fast-paced digital era, small businesses need to stay competitive by embracing technology. The Federal Government has finally approved legislation to enact the Small Business Technology Investment Boost, provided by the Australian Taxation Office (ATO).

In this blog post, we’ll explore how this program can benefit your small business and how to leverage it to maximize deductions.

The Small Business Technology Investment Boost is an Australian government program aimed at encouraging small businesses to invest in technology. It offers an extra 20% tax deduction for eligible assets purchased and installed within the specified timeframe. By leveraging this boost, small businesses can enhance their operations, improve productivity, and gain a competitive edge.

To qualify for the Small Business Technology Investment Boost, your business must meet the following criteria:

You will note that this law is retrospective, covering expenses from 7:30 pm AEDT 29 March 2022 to 30 June 2023 despite only being legislated on 22 June 2023.

This means you will need to trawl back through past spending to capture eligible expenses

The program covers a wide range of technology assets that can help improve your business processes. Some examples of eligible assets include computer hardware, software, printers, scanners, and digital tools. It’s essential to ensure that the assets you plan to invest in align with the ATO’s guidelines to claim the tax deductions successfully.

To claim deductions under the Small Business Technology Investment Boost, you must adhere to the ATO’s instructions and guidelines. It is important to keep proper records of your technology investments, including invoices, receipts, and any relevant documentation. Your tax advisor can provide detailed guidance on how to correctly claim these deductions and maximize your tax benefits.

IMPORTANT NOTE: All eligible spends are claimed in the 2023 business tax return despite teh time frame stretching back 3 months into the 2022 income tax year (29 Mar 22 – 30 June 22).

Let’s consider an example to illustrate how the Small Business Technology Investment Boost can benefit your business.

Suppose you own a small graphic design agency with an aggregated annual turnover of $30 million. You are a small business ✅

In November 2022, to keep up with the latest design software and hardware, you invested $20,000 in new computers, graphic tablets, and design software licenses.

This spend would normally be a 100% tax deduction assuming no private usage of these items.

By taking advantage of the Small Business Technology Investment Boost, you can claim an EXTRA 20% tax deduction in your business tax return. $20,000 x 20% = $4000.

This deduction can significantly reduce your taxable income, resulting in lower tax obligations and more funds available for further business growth.

Assuming you operate a company structure you would save $4000 x 25% company tax rate = $1000.00

The Small Business Technology Investment Boost offered by the Australian Taxation Office presents a valuable opportunity for small businesses to invest in technology and improve their operations. By understanding the eligibility criteria, investing in qualifying assets, and correctly claiming deductions, small businesses can leverage this program to maximize their tax benefits. Be sure to consult with a tax advisor to ensure compliance with all the necessary requirements. Embrace the power of technology and propel your small business towards success in today’s competitive landscape.

The Australian Taxation Office (ATO) recognizes the importance of continuous learning and has introduced the Small Business Skills and Training Boost program

Temporary Full Expensing finishes June 2023. Replaced by Immediate Asset Write-Off with more restrictions.

By linking your myGov account to the ATO, you can now manage your tax and super affairs whenever it suits you.

In ATO online services you can

For details on how to connect MyGov to ATO, visit

If you’re an individual or sole trader, you can manage your tax and super online.

To do this, you will need a myGov account linked to the ATO. To get started, you should have the following.

And two of the following.

If you don’t have this information available, you will need to phone the ATO and get a unique linking code to complete this process.

Once you have this information ready, visit my.gov.au and sign in to your account.

When signed in, go to the linked services section and select view and link services. In the link a service section, select the link button to the right of Australian Taxation Office.

When you link the ATO, myGov will store your name and date of birth in your profile. If you already have a profile, these details must match, read and agree to the ATO terms and conditions. Provide your details, including your tax file, number, name, date of birth and address.

If your details have changed since you last dealt with the ATO, you will need to phone to update them before you can complete the link. Enter information carefully and accurately so that it will match your details held by the ATO.

You will also need to answer two questions from information contained in documents mentioned earlier. If you receive an error message at any time, take note of the error code and follow the link or instructions for more information. Once you’ve finished answering these questions, you’re done.

You have successfully linked your myGov account to your ATO record and that’s it. You can now manage your tax and super affairs through ATO online.

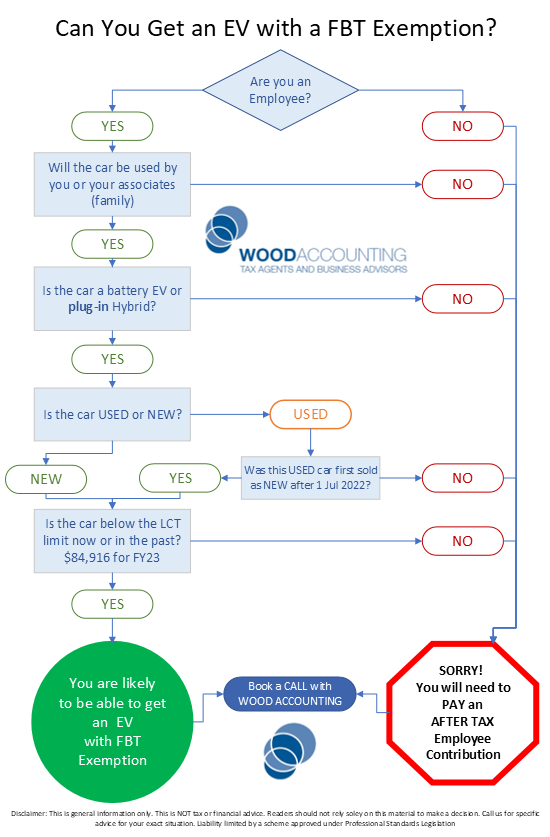

We break it down to explain what fringe benefits tax is, who can get the exemption, and why the Electric Vehicle (EV) exemption is such a good deal.

Federal and State Governments in Australia are now offering incentives to encourage the uptake of zero-emission vehicles. The Federal FBT Exemption is the biggest incentive available at the time of writing this. This can give you roughly a 40% discount.

Did you know you can now get a Tesla for less than a Toyota Corolla?

You need satisfy 3 main elements to qualify:

Assuming you have satisfied the above points you can:

Humans are creatures of habit. Any change comes with concerns but we have found that the benefits of EV adoption far outweigh any concerns people may have.

We have staff who have already taken advantage of this amazing deal so we have real world experience. If you are interested please read the details below.

DISCLAIMER: Please note that the financial examples provided on this page is for illustrative purposes only and should not be construed as financial advice. The figures and calculations used may not be accurate or applicable to your specific financial situation. It is important to seek professional financial advice before making any investment decisions. The author and publisher of this example shall not be held liable for any damages or losses incurred as a result of using the information provided.

FBT, or Fringe Benefits Tax, is a tax system in Australia that applies to non-cash benefits provided to employees or their associates as part of their employment. These benefits can include things like company cars, health insurance, and expense accounts, among others.

FBT is an important part of the Australian tax system, as it helps to ensure that employees are not receiving excessive tax benefits through their employment arrangements. It also helps to maintain fairness in the tax system, by ensuring that all employees are subject to similar tax obligations regardless of their employment arrangements.

When an employer provides a fringe benefit to an employee, they are typically required to pay FBT of 47% on the taxable value of the benefit. However, if the employee makes an employee contribution towards the cost of the benefit, this can reduce the taxable value of the benefit and therefore reduce the amount of FBT that the employer is required to pay.

For example, if an employer provides an employee with a company car, they may be required to pay FBT on the value of the car. However, most workplaces require employee to make an employee contribution towards the cost of the car to eliminate any FBT that the employer may have been required to pay.

Like everything relating to tax, it is a bit complicated.

To get an EV as an FBT Exemption you must meet ALL of the following criteria:

We quickly expand these points below

Good question. Also complicated.

ATO defines Zero and Low Emission cars this as follows:

Motorcycles and scooters are not cars for FBT purposes and do not qualify for the exemption, even if they are electric.

Basically the vehicle must have been first purchased NEW on or after 1 July 2022.

This means the exemption would NOT apply to the purchase of a 2nd hand vehicle that was first used before 1 July 2022.

So to be clear here are 2 quick examples:

This is important.

There must be an Employer – Employee relationship in order for a Fringe Benefit to arise.

The exemption only applies during the employment relationship. I does not apply before or after an employment arrangement is active.

SOLE TRADERS do not qualify as they are NOT employees.

Quick definitions:

Employer = The entity with which an employee has a contract to provide their labour. Written or otherwise. Usually a company or trust which would provide the employee with a payslip, super etc.

Employee = A human who has agreed to work for an entity. Self employed people are included here AS LONG AS they are an employee of their own company or trust.

Sole Trader = Human who has an ABN and works for themselves, issuing invoices for work. Not on payroll. Can’t provide a Fringe Benefit as there is no employee/employer relationship.

To be eligible for the FBT Exemption, the value of the car MUST have been below the LCT threshold for fuel efficient vehicles:

If you buy a 2nd hand EV you will need to get confirmation that it was NOT subject to LCT at any time in the past.

You can check the LCT Threshold for Fuel Efficient Vehicles on the ATO website here

Small Business Owners – If you use a company or trust structure and pay yourself or family wages, talk to us or your Accountant, to confirm that you qualify.

For employees – speak to your HR department or your boss to confirm that you are able to salary sacrifice a novated lease. Then contact the novated lease provider to organise the car.

Sole Traders – sorry, you don’t qualify. FBT does not come into it for you. Your vehicle tax deductibility is assessed by logbook business use percentage.

Mr Wood is looking for a new car. He has rounded it down to 2 of the top selling vehicles in Australia in 2022.

Mr Wood’s circumstances are as follows:

| | Toyota Corolla | Tesla Model 3 |

| Driveaway Price – estimated at Feb 2023 | $36,500 | $67,485 |

| Est. Running Costs – rego, ins, fuel/power, repairs | $5,500 | $4,500 |

| Est. Loan repayments – 60mths, no residual @8% | $8,881 | $12,348 |

| Total Estimated Running Costs Per YEAR | $14,381 | $16,848 |

| ——–ANNUAL PAY AFFECT for Salary Sacrifice——– | ||

| Employee Taxable Income | $100,000 | $100,000 |

| Less: Pre Tax Deduction | ($6,716) | ($16,848) |

| New Taxable Income | $93,294 | $83,152 |

| INCOME TAX WITHELD | ($22,650) | ($19,154) |

| Less: Post Tax Deduction – Statutory Method | ($7665) | ($0) |

| Net Income to Bank – per year | $62,969 | $63,998 |

The above example, using real world numbers, shows that you can get a relatively expensive EV for less than an ICE vehicles despite the drive away price being so different.

Before considering an EV, Mr Wood was earning $100,000 gross income, less $25,000 tax withheld, resulting in him receiving $75,000 into the bank after tax.

Tesla – After pre-tax deductions and tax the income to bank for Mr Wood is $63,998. So compared to the $75,000 above, the Tesla option costs $11,002 out of pocket per year.

This car would have cost him $16,848 after tax had he not salary packaged. $5846 saved per year. This would reduce the cost of the car by more than $29,000 over 5 years. A massive 40%+ saving on the original price of the vehicle.

Corolla – After pre-tax deductions and tax the income to bank for Mr Wood is $62,969. So compared to the $75,000 above, the Corolla costs Mr Wood $12,031 per year.

This would have cost him $14,381 after tax had he not salary packaged. $2,350 saved per year.

So which one is cheaper? The Tesla. Why? This is due to the FBT Exemption. Mr Wood would have a lower out of pocket cost per year.

This is an example so please do your own calculations or ask an expert to assist you to make a decision.

ATO have released a Electric Vehicle and FBT FACT SHEET here if you would like to read more.

Want to discuss your options? Book a call below or send us an email.

DISCLAIMER: Please note that the financial examples provided on this page is for illustrative purposes only and should not be construed as financial advice. The figures and calculations used may not be accurate or applicable to your specific financial situation. It is important to seek professional financial advice before making any investment decisions. The author and publisher of this example shall not be held liable for any damages or losses incurred as a result of using the information provided.